Data centers are the latest buzz in power markets

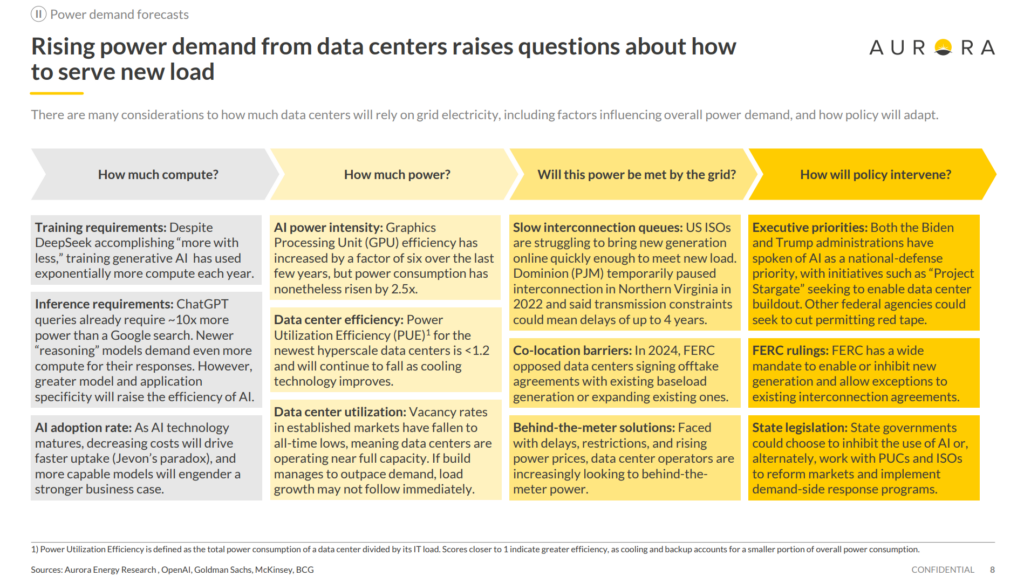

Everyone in power and tech is talking about data centers right now and for good reason. Generative AI has mobilized vast quantities of investment, and large-language models are already altering the knowledge economy. Given its transformative potential, both the Biden and Trump administrations have labeled the development of AI a national-defense priority. Nonetheless, there is still a great deal of uncertainty, not least in considering how such energy-intensive infrastructure will be powered. Chinese tech firm DeepSeek’s January release of its r1 model spooked markets and drove heated discussions of how far their hallmark efficiency gains could be taken. With headlines blaring that data centers will triple their share of US power consumption by 2030, should such computational and training efficiency gains assuage concerns, or will “Jevons’ Paradox” (the idea that as a resource becomes cheaper, the more demand will grow) hold true?

Regardless of how much demand materializes, transmission operators and regulators have been surprised by the prospect of load growth not seen for decades. Publicly available data center forecasts reflect tremendous uncertainty. Amidst regulatory uncertainty and bloated interconnection queues for new generation, do co-location with existing generation or the construction of new behind-the-meter power plants offer a solution for data center developers? Will tech giants stand by ambitious commitments to procure clean energy, or will they walk back climate pledges and spur a gas renaissance? Before examining how the grid could manage this influx of new load, it’s important to understand the different drivers influencing data center development.

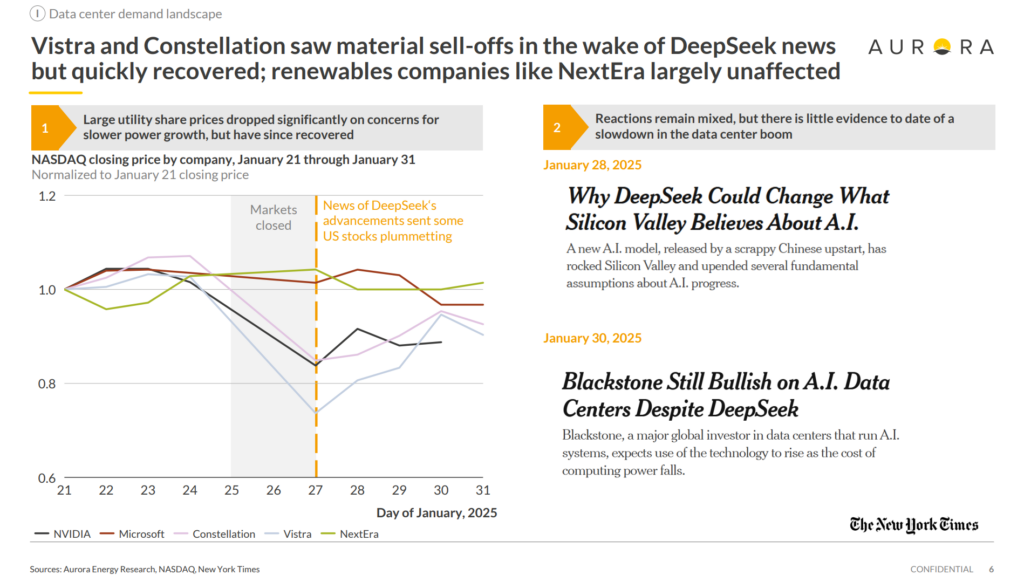

Market reactions to the release of DeepSeek’s r1 model

Data center composition and load drivers

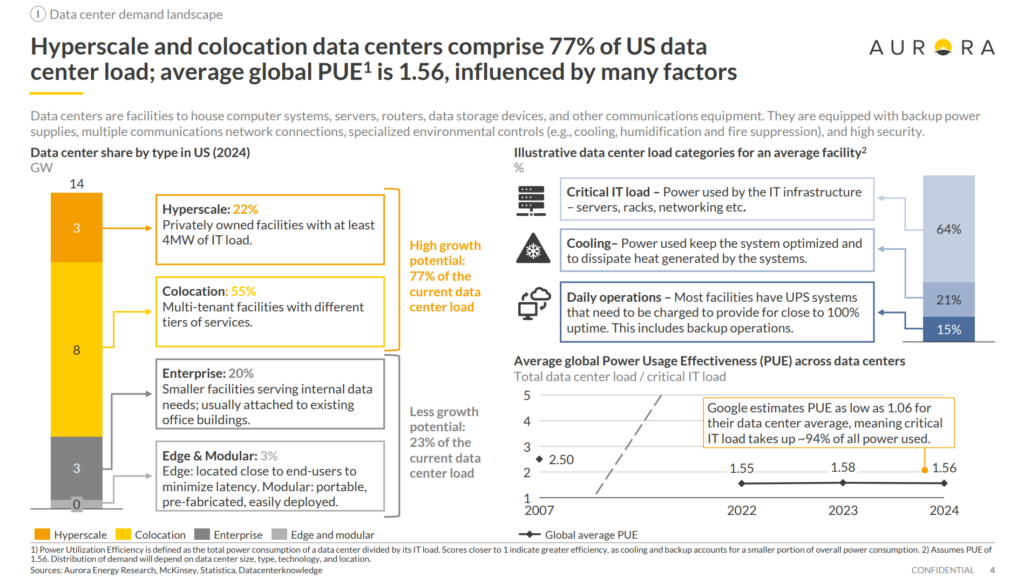

Data centers have been around since the 1940s and now facilitate many daily actions, including syncing cloud-storage softwareprocessing ChatGPT queries, and managing driverless vehiclesDifferent types of data centers serve varying purposes and customer bases. Most headlines focus on co-location and hyperscale data centers: these are expected to account for the majority of growth. While both types serve traditional applications alongside demand for generative-AI inference and training, hyperscalers are best-positioned to capitalize on economies of scale.

As computational workloads have surged and AI-dedicated “accelerator” chips (like NVIDIA’s GPUs or Google’s TPUs) , cooling those systems has raised challenges. For years, national estimates of power use effectiveness (PUE)—the ratio of all power used by a data center to that used specifically for its servers—hovered around 1.5. Recent breakthroughs in cooling high-density server architectures with liquid systems or specialized data center layouts mean that many tech firms’ hyperscale centers, such as those underpinning Amazon Web Services or Microsoft Azure, now boast PUEs at or below 1.1. Conversely, the PUE of most co-location data centers has remained at around 1.6, and their smaller footprints (and budgets) may render it difficult to achieve comparable levels of efficiency.

Data center types and power use breakdown

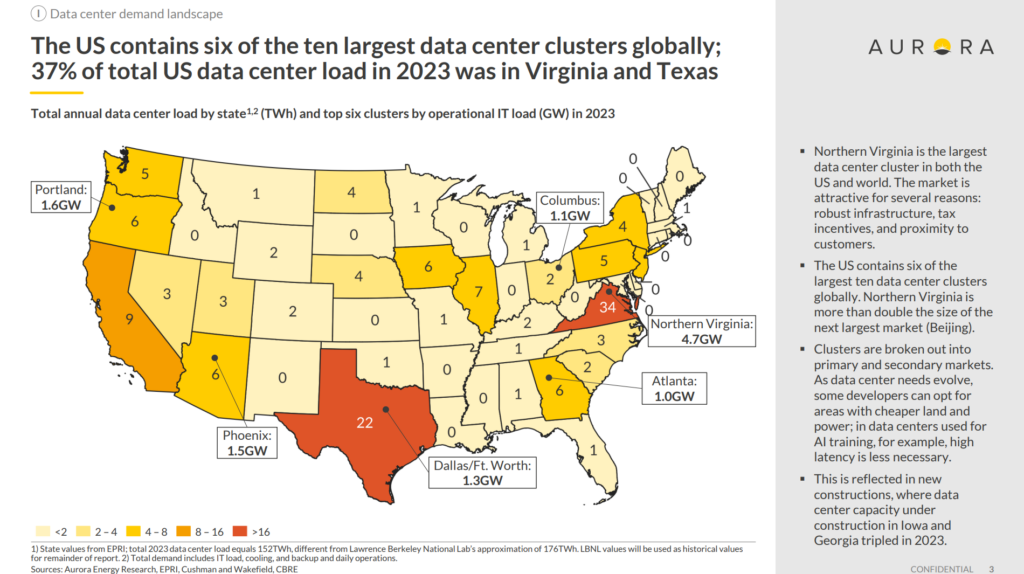

Within the US, Virginia and Texas host an outsized portion of data center capacity. Situated atop robust fiber-optic infrastructure near core customers and galvanized by tax incentives, each of these states alone has seen the construction of more data centers than most countries. Northern Virginia alone exceeds the data center capacity of China’s premier clusters in Beijing.

The accelerating uptake of AI has resulted in data center growth in other states. Cloud computing and corporate data storage require low latency between customers and providers, whereas the training of AI models is more flexible. Burgeoning data center markets in Georgia, Iowa, and Oregon now complement the traditional hubs, and as proximity to Internet infrastructure has become a less binding constraint, data center operators have expanded interest in other areas of the country.

Current data center load distribution across the US

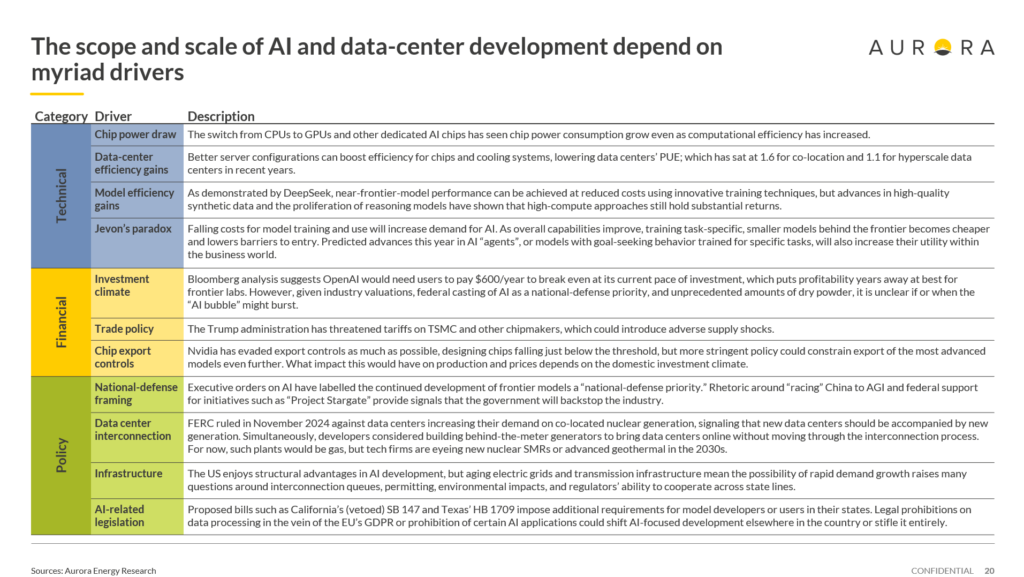

Whether this surge of interest in data center development has real stamina depends on more than the technical case. Even as AI labs draw more power and investment for their work, the business case remains unproven, with revenue streams to support their massive outlay seemingly years from materializing. . While gains from falling costs promised by Jevons’ Paradox could accelerate the development of other parts of the AI value stack, turbulent economic conditions could still halt the AI revolution before the benefits of the technology are widely realized. Uncertainty around federal trade policy and chip export controls provide a foretaste of the challenges to come as rhetoric around an “AI race” with China heats up in Washington and Silicon Valley alike.

On the regulatory front, decisive action (or a lack thereof) will shape the development of power markets for the coming decades. Even as presidential directives spell out the importance of investment in America’s infrastructure, interconnection queues across US power markets remain bloated, forcing developers to consider shortcuts. Developers’ plans to sign offtake agreements and co-locate with existing nuclear or gas plants hit a snag last November when FERC ruled against Amazon’s proposed expansion of such an agreement in Pennsylvania. Tech firms instead have examined the viability of building their own power plants alongside data center complexes to sidestep the grid entirely. The timeline for such a solution poses challenges: speculative technologies, such as nuclear SMRs, will be years more in development while supply bottlenecks for gas turbines diminish their viability as an interim solution.

Non-exhaustive list of drivers of data center demand

What goes into a data center load forecast – and are they realistic?

When viewing electricity demand forecasts from data centers, it’s impossible to backtrack exactly how forecasters may have arrived at this value from growth in IT capacity. Consider the following:

- Energy efficiency as measured by PUE (how much power a datacenter uses on cooling, backup, and daily operations relative to actual IT load); several factors could affect this, like cooling efficiency gains

- Computational load factors.

- Vacancy rates

- Behind-the-meter (BtM) generation; this would serve the data center load directly and could reduce grid strain though regulatory uncertainty challenges the feasibility of BtM solutions

- Type of data center by market (hyperscale , co-location, modular, edge) and application (AI training, AI inference, non-AI); how growth in data center markets evolves over time would influence the above factors

Factors determining how much data center load will grow, and how much will be served by grid

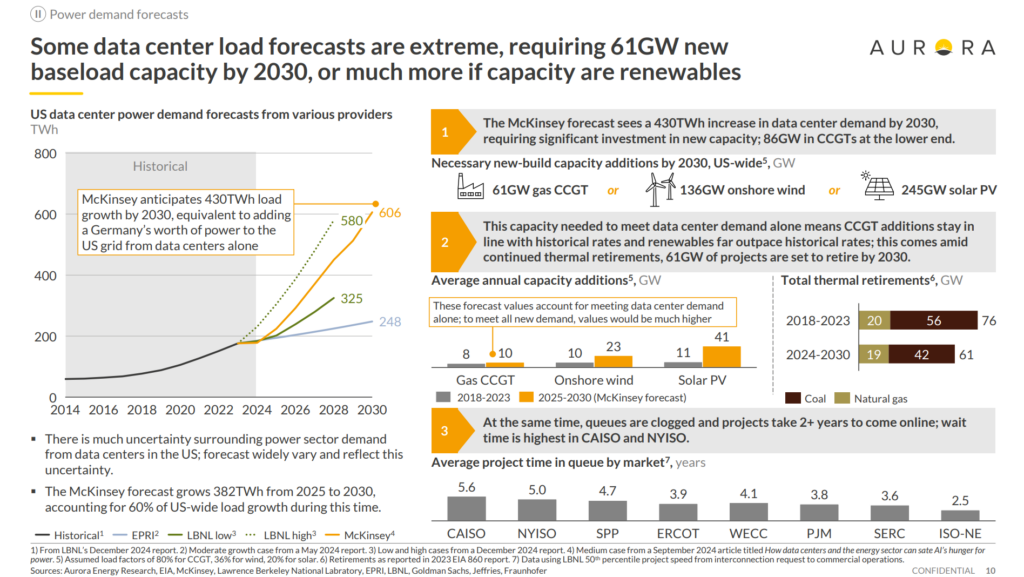

No matter how you arrive at the total load figure, there is little consensus on how market analysts and academics expect total electricity demand from data centers to evolve over time. According to publicly available US-wide data center demand forecasts, the values range from 248 TWh to

606 TWh data center load by 2030. The difference between which is effectively the annual electricity consumption of seven New York Cities.

Looking at the most extreme “medium case,” the new power needed to supply this influx of data center demand would be incredible—equal to the production from 61 GW new gas CCGTs, 136 GW new onshore wind, or 245 GW new solar PV. Given that data center demand shape fits best with baseload generation, there would need to be 10 GW annual additions of new CCGT capacity through 2030 to fulfill the demand . This 10 GW exceeds the historical rate of CCGT additions. Furthermore, it only accounts for growth in data center demand—not including other demand growth from continued population increases, electrification, and onshoring manufacturing.

Data center load forecasts and necessary power supply

Of course, in reality, it takes time for new generation to come online (either behind or front-of-meter). Based on our analysis, we expect that as quickly as these data centers can come online, we will see higher load factors for gas and coal plants and (very locationally dependent) less renewables curtailment. Whether data center load will reach the 606 TWh figure by 2030 remains to be seen. This is not the first time—and certainly won’t be the last time—forecasters are inevitably proven wrong. Take predictions of “peak oil” by the 2000s, forecasted demand explosion from the widespread use of the internet, or projections of a 100% nuclear energy-powered system in the 1970s. Grid load from data centers will be driven by multiple factors whose trajectories are unclear, including technological developments, consumer patterns, and policy response. The statistician George Box said, “all models are wrong, but some models are useful.” It’s like forecasts—understanding the different drivers and what impact they may have on grid load from data center will be crucial in order to understand the impact growth in AI and data center load may have on power markets.

Authored by:

Lizzie Bonahoom – Research Associate

Callaway Sprinkle – Senior Analyst