We provide decision-makers with actionable intelligence

to navigate and capitalise on the global shift in energy systems.

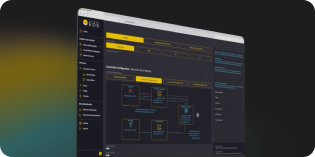

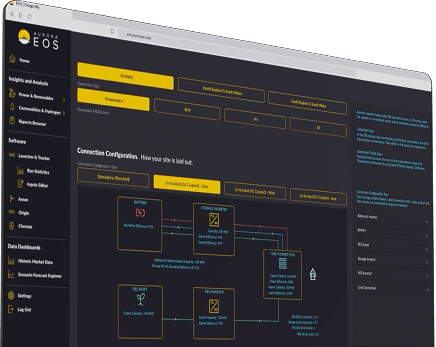

EOS Platform

EOS is Aurora’s integrated energy intelligence platform, bringing together forecasts, market models, reports, and tools to support strategic decision-making.

Software

Our software suite enables energy professionals with advanced tools for market forecasting, asset valuation, and strategic decision-making.

Subscription Analytics

Access energy forecasts, policy insights, and analytics tools designed to inform smarter, faster market decisions powered through our subscription analytics.

Advisory

Bespoke advisory support combining deep market expertise, modelling and insight to help clients navigate complex energy investment and policy decisions.

Aurora Energy Research has consistently provided us with exceptional insights and data-driven analysis, helping Vattenfall navigate the complexities of the energy market. Their expertise and detailed market forecasts have been invaluable in supporting and shaping our strategic decisions and long-term planning.

Martijn van Gemert

Director Market Insights, Vattenfall

Clients

+

Countries

+

Transactions

+

Advisory Projects

Strategic market focus

for your sector

Financial Sector

For informed capital allocation in evolving energy landscapes, energy investors trust Aurora's analytical rigour and regulatory expertise.

Energy Consumers

Large-scale businesses optimising energy procurement, balancing cost-efficiency, reliability, and sustainability while meeting operational and regulatory requirements.

Utilities

Organisations managing energy generation, transmission, and distribution, optimising grid performance and integrating renewables to meet future energy demand.